November 2, 2020

How to get it right from the start

Planning to launch a fintech app? Right now, the time (and market) is just right for sleek, mobile offerings that facilitate financial transactions and cut costs for both users and operators. So, whether you’ve come up with a cost-effective way to connect borrowers and lenders, an easier way to pay or split the bill, a targeted, tax-saving offer for freelancers or simply an update to your own banking services – A fintech app could be the way to go.

To make sure you get this right from the very beginning, we’ve created a series of articles to guide you through the entire process, from legal constraints and considerations (this feature) to technical recommendations, vital customer insights and the latest trends and technologies destined to shape the future of fintech.

Expertise you can trust

YND has been building fintech applications and software since day one (2014), driving the early wave of disruption in a remarkably traditional, resilient and heavily regulated market: financial services. Over the years, we have designed and delivered numerous successful fintech solutions. From nimble start-up to international heavyweight, for clients across the globe in Europe, South America, Asia and Australia.

Idiosyncratic customer behaviours, special security issues and national and international red tape have made this a uniquely challenging, yet also uniquely rewarding, journey. It’s one where we have learned a lot on the way – resulting in valuable knowledge and expertise we want to share with you, to ensure your fintech planning avoids some of the most common pitfalls.

Know the legal framework and stipulations

Can’t wait to get started on your outstanding project? Hold your horses: there might be a good reason as to why it hasn’t been done yet. You can’t just start issuing loans, cards or currency - and some necessary steps might complicate customer onboarding and retention. Here are the main points you should first consider:

Start with an analysis of potential competitors in your chosen market

If something seems “overly complicated”, this is probably not bad UX or uninspired product design, but something required for compliance.

Make sure you’ve contemplated all aspects of your product. Are you targeting private users or businesses? Small or large companies? All this can affect your legal requirements, so when looking at competition, take this into account.

Even a seemingly low-level app might require very specific permits or even an e-money or full banking licence. So, before you start, make sure you research and fully understand all regulatory requirements that apply to your chosen market, from obvious financial frameworks to data protection and privacy requirements.

A smooth sign-up is always a challenge

While it would be great to offer prospective clients a smooth one-click onboarding experience, fintech or banking solutions usually require further steps and stringent identity verification processes.

Sign-up requirements for similar services might differ significantly across markets due to national anti-money laundering or know-your-customer provisions, among others. Hiring a local expert to clarify all applicable rules is usually money well-invested.

You will need to ask prospective users to provide a lot of data - and then also verify whether this data is valid. There are several ways to streamline this process:

- Only request information that is absolutely necessary. Marketing, demographics and other nice-to-haves can wait.

- Don’t ask twice for data you have already collected, or for information that is accessible via open / government services like Financial Conduct Authorities in the UK, Australian Prudential Regulatory Authority, Credit Bureau Singapore, and so on.

- Use know-your-customer services like IDNow, WebID, Onfido and others to speed up verification of customers identity that is required in many jurisdictions in the EU and UK.

- Instead of asking for the uploading of bank statements, you can leverage the PSD2 regulations in EU and similar Open Banking provisions in other countries to employ services of financial data aggregators like Plaid, Yodlee in US or Tink, FintecSystems, Kontomatik and others in EU. Here’s a handy list of services provided in different markets.

Last but not least, the amount of data required might also depend on specific risk assessment criteria (i.e. for loan or insurance products). Or it could be a business decision — is it worth taking more of a risk to offer a smoother experience than your competitors?

Privacy laws are not to be trifled with, especially the European Union GDPR

Please remember that the European data protection regulations may affect your business, even if you don’t maintain physical operations within the EU. To ensure compliance, you will need to document processes and policies as well as regularly review your security measures – and ensure all of this is designed into your app.

These regulations also stipulate that you should only collect and process personal data for a specific, business-related and required purpose (the ‘data economy’).

Your customers have the right to data portability (i.e. the right to switch service providers and to request a record of their personal data held on your servers). Any breaches need to be communicated to the relevant EU authorities within 72 hours.

Don’t treat the regulators involved as a necessary evil

A fake it till you make it approach is absolutely not recommended in fintech. While many regulations add to the workload, they exist for good reason – mostly to protect consumers and their savings.

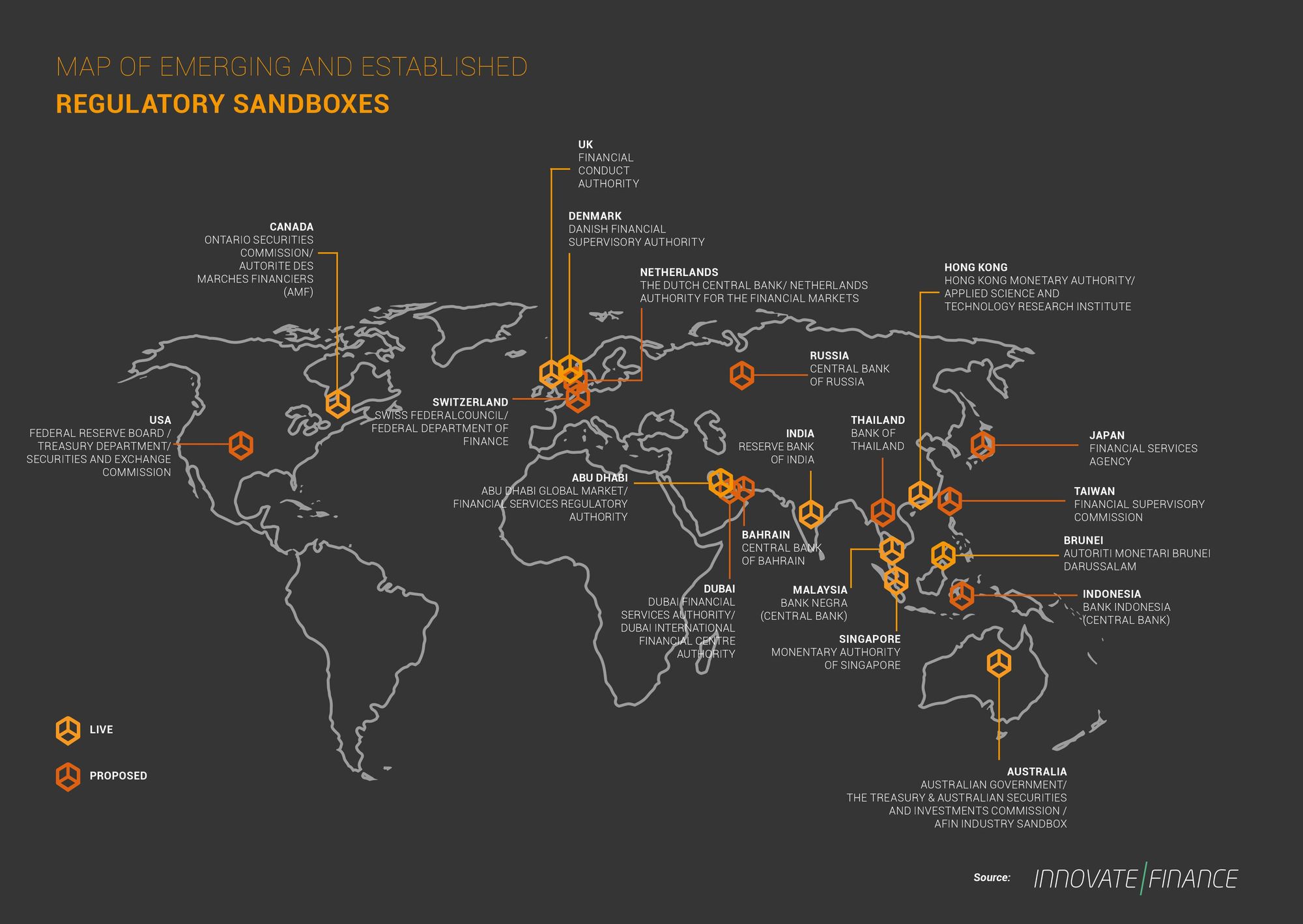

Playing fast and loose with such regulations can have dramatic consequences for your business, from steep fines to expensive litigation. The law can also be your friend: In many countries, regulators actively support fintech start-ups by setting up regulatory sandboxes. While small, nimble players can use these to road-test their solutions in a safe environment, regulators gain valuable insights into how to shape future provisions that keep up with fast-paced innovation.

Source: Industry Sandbox

Sometimes, legal constraints are not obvious at all

Make sure you read the fine print, even if your project isn’t obviously finance-related. Loyalty schemes, for example, that reward customers with points to be spent on the platform, may be treated like a currency and require an e-money licence or similar – depending on the specific jurisdiction and loyalty scheme design. Once again, we recommend consulting a seasoned expert BEFORE you start on design and development.

Start small and focused

Can’t see the wood for the (regulatory) trees? In fintech, a modular, step-by-step approach starting with core functionalities can work wonders to avoid unforeseen complications down the road. If, for example, your target audience is businesses, you could start with specific company types that have similar legal forms and frameworks.

Finding the right partner is key - here’s how to do it

Choose partners with a strong fintech track record (in your relevant market)

Not every software development company has sufficient skills and expertise to navigate this tricky field. While technical and design chops are an obvious must, a partner with proven fintech experience will help you avoid serious stumbling blocks and bring your product to market faster.

Prepare for an intense exchange: A great partner will also pepper you with questions from the get-go and challenge your assumptions to ensure that the results really meet your expectations. Service providers that simply say yes to all your wishes and proposals are more likely to derail lofty plans further down the road.

Look for partners with a proven track record of actual deployments, not slick mock-ups and presentations

Flashy banking interfaces are a dime a dozen on dribbble. Almost all of them are just that, though – pretty images with no substance and certainly no real-life application. Be sure to choose a partner with an evident history of delivering successful, real-life results.

Embrace collaborators

Due to the fast-paced, novel and ever-evolving nature of this budding market, it’s unlikely that one single partner will cover every area of expertise. Keep an eye out for partners who have no problem telling you, “We don’t know… but we know exactly who can help with this”.

At YND, we appreciate (and frequently rely on) our long list of domain experts and potential collaborators; a network assembled through countless projects in the field of finance. After all, it’s the result that counts – and the right mix of people behind it.

Ready to jump right in?

If you’re serious about turning your digital fintech visions into tangible reality, we’re here to provide expert guidance, and to take care of the implementation. Thanks to our extensive experience in the world of fintech, we know the legal provisions by heart – and how to navigate any potential hurdles.

Feel free to get in touch to discuss the details – and look out for the next instalment of our series on how to get your own fintech off the ground.

This post was written by Paweł Nowotarski, Creative Director and fintech expert at YND. In need of some brain power? Reach out to us via hello@ynd.co with questions about your projects.